Health Spending Rebound Continues into June Amidst Economic Devastation and New Covid-19 Fears

July 30, 2020

With yesterday’s release of U.S. gross domestic product (GDP) data for the second quarter of 2020, dire economic anxieties were confirmed as we saw the worst reading in the series’ history (which goes back to 1947): a drop of 32.9% at a seasonally adjusted annual rate. For the quarter, covering April thru June, health care services accounted for 9.5 percentage points of this total decline, or about 29%. This morning, the U.S. Bureau of Economic Analysis released data on Personal Income and Outlays, giving us a first look at June-specific data. It showed that the rebound we have been tracking in personal health care spending has continued: while April was down a whopping 29.0% and May 16.5%, June spending was down only 7.5% – all compared to the same month in 2019. In this perspective, we update our Health Sector Economic Indicators framework to analyze health spending and selected components, and consider various prospects over the short- and medium-term as Covid-19 continues to ravage the country.

June 2020 Health Care Spending Data

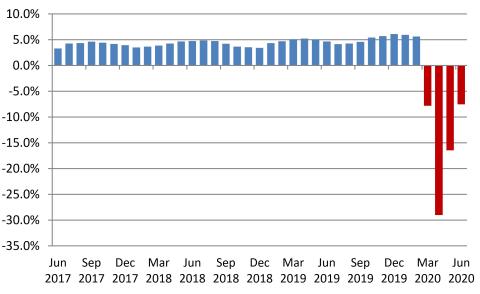

Exhibit 1: Year-Over-Year Growth Rates in Personal Health Care Spending

Exhibit 1 clearly shows the recovery, after February, of personal health care spending. Of note, June’s year-over-year fall of 7.5% is slightly less bad than the March reading of -7.8%, and thus the smallest year-over-year decline since the pandemic struck.

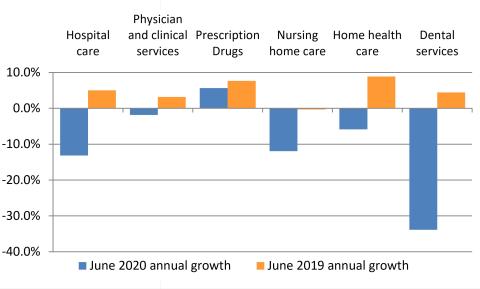

Exhibit 2: Health Spending 12-Month Growth for Major Categories

Exhibit 2 decomposes total personal health care spending to illustrate 12-month changes for six categories, both for June 2020 and June 2019. Considering June 2019 annual growth as a baseline, it is interesting to see the range over which the categories have returned to the earlier growth rates. On one end of the continuum is physician & clinical services that have recovered to being down by only 1.9% compared to a year-earlier growth of 3.2%. On the other end of the continuum is dental services, still down 33.9% compared to the 2019 growth of 4.4%. In the middle is hospital care, down 13.1% compared to 5.0% growth in 2019. The prescription drugs category is the outlier, never going negative during the pandemic, although it has fluctuated from a high annual growth of 12.7% in March due to people stocking-up, to a much lower rate of 3.8% in May and now 5.6% in June.

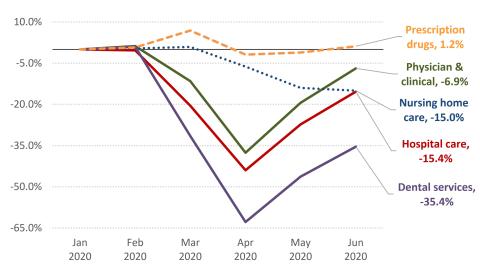

Exhibit 3: Cumulative Spending Growth since Jan 2020, by Major Categories (Percent Difference for Jun 2020 shown in data labels)

Rather than “starting the clock” in June of 2019, Exhibit 3 pegs the baseline at the beginning of the year and traces spending recovery for five categories on a cumulative basis. Most of the major health spending categories follow the trend seen in hospital and physician & clinical spending, having bottomed out in April 2020 and then recovering in May and June, but still significantly below their February pre-pandemic levels. The long road back for dental services (down 35.4% cumulatively) is also seen in the cumulative data, having taken the most extreme hit from delayed care during the pandemic. Nursing home care spending avoided the initial severe drops in spending early in the pandemic; however, it is not recovering at all – its continued deterioration leaves its spending at -15.0% compared to January 2020. As mentioned above, prescription drug spending has only seen modest changes in 2020.

A Macro-Economic Update

While huge attention was appropriately directed to yesterday’s historic GDP decline, lost in the commotion is the two-week string of deteriorating labor data as indicated by unemployment insurance weekly claims showing 1,434,000 initial claims for the most recent week. Worse, so-called continuing claims are back above 17 million, and total claims, counting the new special programs, exceed 30 million! A new Census Household Pulse Survey, for July 16 to 21 period, shows the number reporting not working is moving back down again but still below the recent “recovery” peak in mid-June. The number reporting not working because the company went out of business or they were laid off continues to rise. Official labor data from the Bureau of Labor Statistics for the month of July will be available August 7th.

Today, the University of Michigan Consumer Sentiment Survey shows a decline of 25% from the same period in 2019. But most worrying of all the cross currents is the delay over new Federal stimulus legislation. The data clearly show that, despite massive declines in economic activity and consumer spending, incomes have been mostly stabilized and actually slightly up, because of previous legislation, especially the CARES Act. With no legislative compromise for continuing this help in sight, it creates a scary macroeconomic cliff if a deal is not found soon to renew extra unemployment insurance and other federal supports for those unable to work or otherwise missing incomes.

Looking Ahead

It is worth repeating that, like so many unprecedented current events, we have never had an economic downturn that was abetted by the health care sector. In all post-World War II recessions, health provided a stabilizing function, that is, it cushioned the blow from declines in the other sectors. Not this time. A few months ago, when health care spending dropped sharply but there was solid hope for quashing Covid-19 infections, we would have confidently predicted a continued recovery in health care spending and, perhaps, even an increase to account for pent-up demand. But with new cases steady at about 65,000 per day, the daily death count at nearly 1,200 and rising, plus a revised projection by IHME of 230,822 deaths by November 1 (up from 219,864 projected on July 22), it is likely that economic progress will stall. Health care activity can also be predicted to follow suit as fear of receiving care regains the upper hand. We are especially concerned about life and death care that is not received. Emergency room visits are down sharply (though they have recovered of late), and there has been a drastic decline in health screenings with models predicting “delayed diagnoses of an estimated 36,000 breast cancers and 19,000 colorectal cancers due to Covid-19’s scrambling of medical care.” Most amazingly, 1 in 4 survey respondents said they would rather stay home out of fear than go to a hospital when experiencing a heart attack or stroke!

We wish to highlight three related issues:

- While the data indicate a high plateau for many areas in the country, will ongoing Covid-19 infection spikes in other parts of the country naturally cause concern if other states may become the next Arizona, Texas, or Florida? Further, will opening schools have a major impact on community spread now that we are learning children may carry the virus at high levels?

- Will the reversion to normal health care spending be below or above trend? In some parts of the country, for example New York and Massachusetts, we’ve now seen suppressed Covid-19 spread for a couple of months. How quickly will care come back and is there truly pent-up demand that will result in “catch-up spending” this fall? Or, will health spending only return to trend, leaving a permanent hole in 2020 revenues from the spring?

- While we’ve emphasized macroeconomic factors, it is worth calling out the effects of this calamity on state budgets which are being decimated by evaporating revenues, yet are also faced with unique spending needs, especially Medicaid expenditures. There is the strong potential of a vicious cycle of state and local spending cuts, lost jobs and the impact on declining commercial health insurance, among other effects, especially if support for state and local budgets is not included in the next round of federal monies.

We will, of course, continue to closely monitor the spending, employment, price and utilization data. Specifically, we will analyze new total and health care employment data to be released on Friday, August 7th.

Altarum’s health sector tracking work is made possible by a grant from the Robert Wood Johnson Foundation.